For 40,000 years people have used rare objects as a form of currency, bartering to get prized possessions. When the first coins appeared in Mesopotamia 5000 years ago, it rapidly facilitated the exchange of goods, enabled gift-giving and gave states power.

Over the millennia money has become synonymous with success and well-being — but without scarcity, money can’t be controlled, and therefore the people can’t be controlled either.

Those who had money had power, and much like today they used that power to enrich themselves further — Aristotle was a known critic of his time, despising those who make “a profit from currency itself, instead of making it from the process which currency was meant to serve”. Usury, the practice of lending money at extremely high interest rates, became common practice, and lending and borrowing is just as common today. Everyone knows about it in the real world — if you lend money you get paid interest and if you borrow money you pay interest. Simple. But access to reasonable rates is difficult and some people have no access at all.

We live in a debt-based economy, where money is created out of thin air and debt is required to sustain the system. In the fractional reserve banking system only banks can create and destroy money but other entities can lend it. This leads to the following problem: money supply can’t increase unless debt increases, but debt can increase without an increase in money supply. This system is unsustainable! So what about crypto?

Crypto Lending

Crypto can be loaned or borrowed from many different places, some of which are centralised and some of which are decentralised.

If you look at a Nexo or a BlockFi, these companies act a bit like crypto banks. They make their money not only with retail but also be lending out funds to institutions and exchanges, for example for leverage trading. You’ll be able to get high single-digit annual returns on your stablecoins and low single-digits on other crypto, but at the end of the day you are still trusting a central body to manage their loans properly. It is worth checking whether they are insured and/or properly regulated.

DeFi is where it gets interesting. There are several protocols that allow you to deposit your tokens to earn interest or borrow tokens while paying interest. One of the key improvements here is that your wallet interacts directly with the protocol so you have full custody of your assets, as well as the additional privacy of not having to sign-up with a central entity.

Like swapping tokens on a Decentralised Exchange (DEX), lending and borrowing protocols work with smart contracts to allow you to deposit or lend tokens from a pool via automated process. It is the use of these smart contracts that removes the ‘trust’ element of centralised offerings, with one exception: the smart contract and associated oracles have to be solid and good auditing is of paramount importance.

How does it work on DeFi?

There are many DeFi protocols out there, including Aave, Compound, Maker, dydx etc. Let’s use Aave protocol as an example — how does lending work?

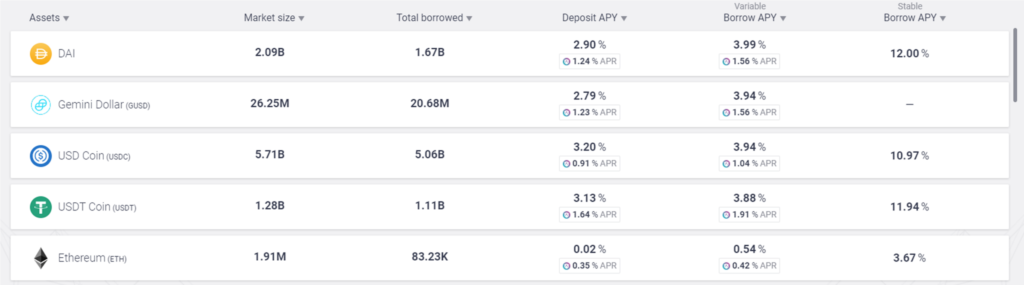

You simply need to go to the protocol’s website and connect your wallet. Then you can browse the markets that you can deposit into and see the current interest rates. The image below shows the top 5 on listed on Aave today:

If you deposited USDC into the Aave market your interest rate would start at 3.20% — but note that this is a variable interest that changes depending on the supply and demand of the market. In return for your deposit you receive aUSDC tokens, which are effectively an Aave voucher to prove that you own the tokens you sent to the pool. It is these tokens which accumulate the interest over time until you redeem them.

If you want to borrow USDC there are two interest options — either a lower, variable rate or a higher, fixed rate. The interest rates can change with every Ethereum block validated and the rates can fluctuate quite a lot, so it comes down to appetite for risk. Where crypto lending tends to differ from bank lending though, is that the loans all tend to be overcollateralised — meaning, you have to deposit more funds than the loan you wish to take out. This might seem crazy — I mean, why borrow $750 if you’ve already got $1000?

It’s because of two things:

- You can get access to cash without selling your crypto, if you think the crypto will rise in value

- You can potentially avoid capital gains taxes (by not selling your crypto and taking out a loan)

In the world of crypto there are some additional attractive features:

- Your collateral can be in one token and you can borrow a different token

- You can find another way to make a good yield on the tokens you borrow

For example, I could deposit USDC earning 3.2% interest and use it to borrow ETH at only 0.54% interest. I could then use that ETH to provide liquidity to another protocol that perhaps earns me 8% in transaction fees, which would boost the overall interest rate on my original collateral to closer to 9%.

Is it Unlimited?

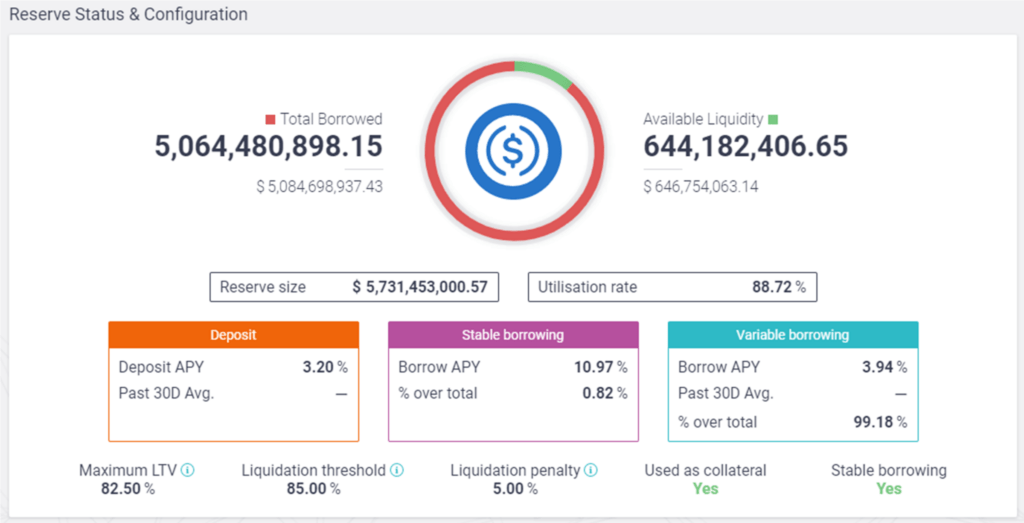

The amount you can borrow is not unlimited. When you click on a market you will see a few pieces of important information — Aave example given below:

- Available Liquidity — you can only borrow what is available in the pool

- Maximum LTV — Loan to Value ratio. For USDC the ratio is currently 82.5%, meaning if the user has deposited 1 ETH as collateral they can then borrow 0.825 ETH in USDC. If the debt in USDC becomes more than the LTV multiplied by the total collateral then a ‘margin call’ is made, where the protocol alerts you to give you time to add additional collateral to restore the LTV to below this maximum.

- Liquidation Threshold — when the debt is worth more than this value multiplied by the collateral value. To continue the example, when the debt in USDC becomes more than 0.85 ETH due to fluctuating ETH prices. At this point the collateral is used to pay off the debt, at least until the LTV is below the maximum value.

Other protocols like Compound and Maker work on similar principles — the aim of the game is to put your loans to work while avoiding liquidation. If you have several tokens loaned and borrowed on several platforms it can get quite tricky to track, and there are some dashboards, such as DeFiSaver that can help you manage it all in one place and lower the risk of inadvertent liquidation.

Optimisation

All of the protocols mentioned up to now are based on ERC-20 tokens, and what does that mean? GAS!

Gas will usually dominate the fees but some protocols charge a transaction fee for borrowing. For example Aave charges 0.01% (unless you’re taking out a flash loan — more on that below — in which case it’s 0.09%).

As you might expect, lending protocols are showing up on Ethereum Layer 2 solutions (such as dydx) and other blockchains now in order to (almost) eliminate gas fees. The newer protocols often have some of the best interest rates because they have low liquidity and the supply-demand algorithm rewards early joiners for their support — but this of courses comes with more risk.

As you may have picked up, the lending of stablecoins dominates the market, and this is because their value is pegged to fiat and is seen as a lower-risk asset that can have high LTV ratios. There are then two other, more advanced, options that can help to keep fees low:

- Yield Optimisation — for example Yearn.finance, which has vaults of stablecoins that the smart contract automatically shifts around to different lending protocols depending on where the highest interest rates are.

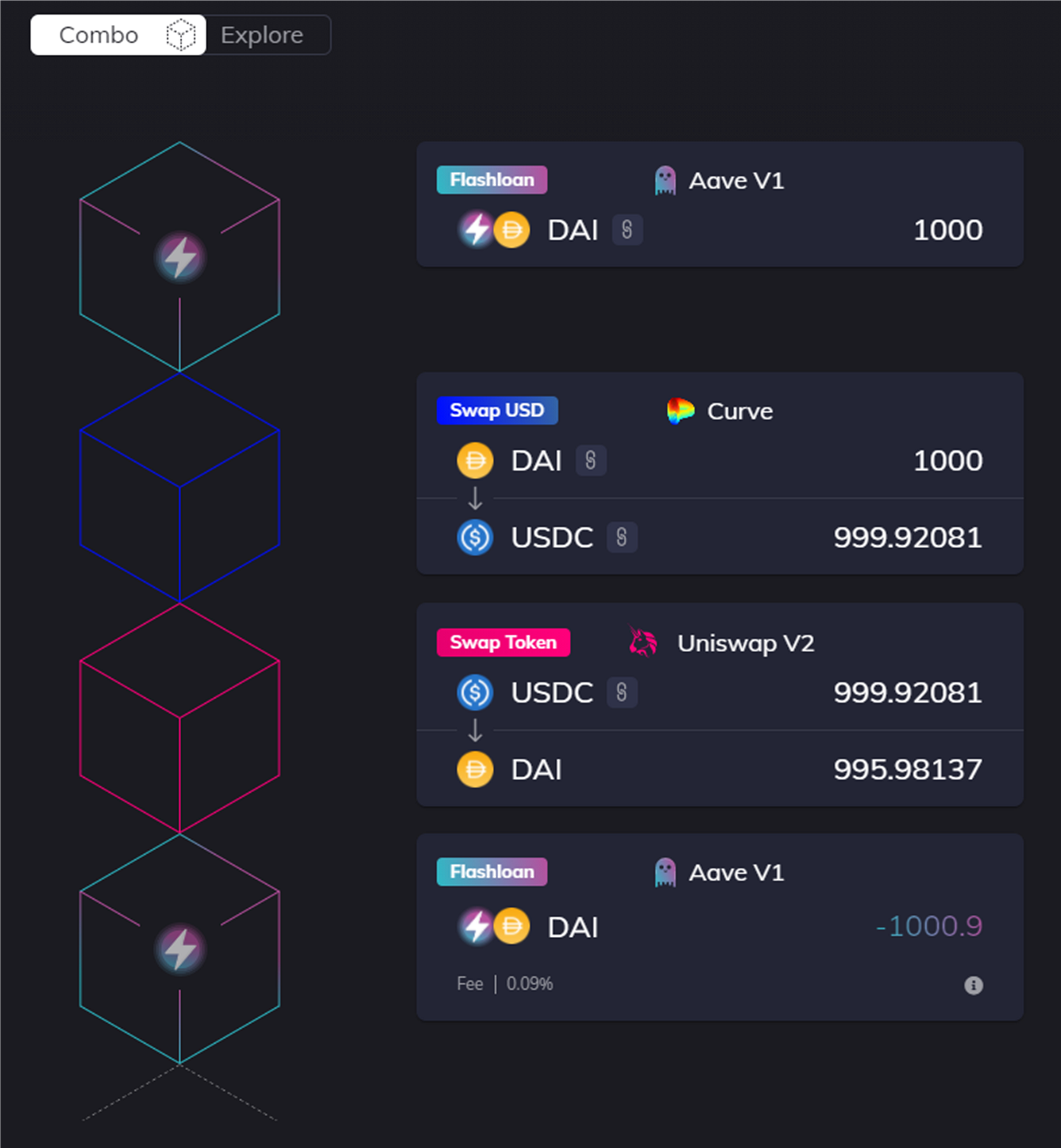

- Flash Loans — by bundling several actions into a single Ethereum transaction you can borrow without collateral, use it to generate interest and repay the loan before the transaction is validated. If the loan is not repaid the transaction is cancelled as if nothing happened.

Flash loans are historically the playground of coders but if you want to try it out for yourself you can check out Furucombo (still in beta — use at your own risk), which lets you select and arrange a multi-step transaction, like the one below (although this one wouldn’t make money with the current rates).

Concluding Remarks

Crypto lending can be a lower-risk approach to earn single-digit (sometimes double-digit) returns, predominantly on stablecoins — if you’re looking to diversify, this might be a method of passive income for you.

And if you dive down the rabbit hole, there are several more advanced strategies that you can investigate to maximise your yield and keep compounding that interest. But do your own research on the protocols and don’t go all in. You want to be able to survive if one of them goes bust.